A Look Into the Markets - April 12, 2025

"You Dropped a Bomb on Me" – You Dropped a Bomb by the Gap Band.

Consumer Prices Climbing

On Wednesday, the Consumer Price Index (CPI) was reported, and all measures came in higher than expectations. This means that the headline number which includes food and energy was higher, the core reading which is inflation without food and energy was higher and the month-over-month readings and the year-over-year readings were higher. How high? The headline number came in at 3.5% year over, which is up from 3.2% from February. CPI bottomed last June at 3.00%.

This is a very important story to follow as inflation is a main driver of long-term interest rates. So, this higher-than-expected reading was very unwelcome and unnerved the markets to start the day.

Adding to the uncertainty and volatility, was recent speculation that the disinflation process or slowing rate of inflation was well at hand. The CPI reading coupled with last month's higher numbers has removed that comfort. With oil prices also at 2024 highs, we have rising fears that inflation will go higher still, which would likely mean higher rates.

Bye-Bye June Rate Cut

The renewed inflation fears have the markets pricing in no chance of a Fed rate cut in June. Right now, the markets are seeing the strongest possibility of a cut in November. This is a major change from when we started the year, as the financial markets were thinking the Fed would cut rates six or seven times, and the Fed said three. Now we could very well not see a rate cut in 2024.

The Fallout

On Wednesday, just hours after the CPI reading, the Treasury Department had to sell $39B worth of 10-year Notes. How would this auction go after a high inflation reading, fears of more inflation, and continued deficit spending? Well, the auction was awful. The Treasury had to issue higher interest rates to attract investors, due to tepid demand. This added to the pressure on rates and pushed the 10-year Note and thus mortgage rates to the highest levels of 2024.

The Fed Minutes

Two weeks after every Fed meeting, the Fed releases their Minutes, which are bullets of what was discussed among members. These are released to give financial markets a peek at what they are saying behind the scenes. Note, these Minutes are carefully packaged to help guide markets. We will not see the full Minutes from these meetings for five years.

The Minutes were about as bad for the mortgage industry as they could possibly be.

Half of the bullets released talked about fear of inflation, persistent inflation, and uncertainty that it will come down. This was not part of the Fed meeting two weeks ago where the Fed Chair Powell led the markets to believe that three cuts were still coming and that inflation was trending in the right direction.

They also said that they want to start slowing the balance sheet reduction, but only in Treasuries and not mortgage-backed securities. This was also unwelcome as the spread between mortgage securities and Treasuries is historically wide and could narrow considerably if mortgage-backed security balance sheet reduction was slowed.

4.50%

This is an important level to watch in the 10-yr Note. For mortgage rates to find their footing and see improvement from this past week, we need to see the 10-yr Note move back beneath 4.50%.

Bottom line:

This past Wednesday, changed the landscape for interest rates as we head into the home buying season. With inflation fears elevated, the Fed backing away from a June rate cut, and Treasury auctions not performing well. It is tough to see where the relief in interest rates would come from in the near term. We will need to listen carefully to incoming data on signs that the inflation rate is cooling.

Looking Ahead

The tone has been set with rates higher for longer. Now we will be receiving some moderate impact reports and a bunch of Fed speakers. The latter of which has been sharing that less Fed rate cuts are on the table. And with last week's news, why would you say anything different?

Mortgage Market Guide Candlestick Chart

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 6.0% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa.

If you look at the right side of the chart, you can see how prices have touched the lowest levels of the year, representing the highest rates of 2024.

Chart: Fannie Mae 30-Year 6.0% Coupon (Friday, April 12, 2024)

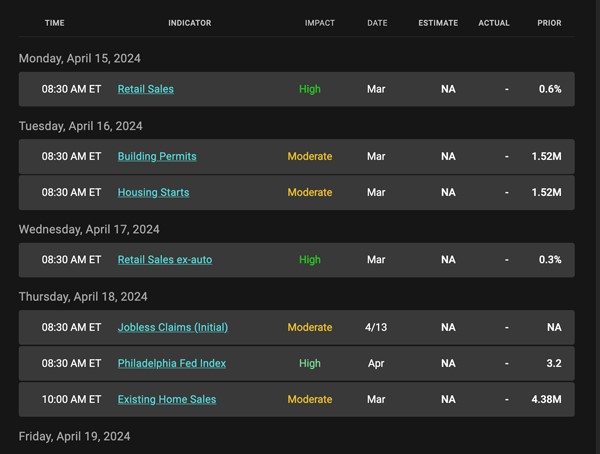

Economic Calendar for the Week of April 15 - 19

|

|

Categories

Recent Posts

concierge@pennergroupproperties.com

16037 SW Upper Boones Ferry Rd Suite 150, Tigard, OR, 97224